Auto Loan Fraud is a big problem here in the US and growing. Annual estimates are that approximately $6 Billion in car sales are made and financed with a loan containing some fraud on the application.

That is a big number. And lenders are looking for any ways that they can reduce that fraud. Many are turning to the car dealers to be their first defense against fraud. Since the car dealer has the borrower right there in front of them, they are often in the best position to stop the fraud.

Here are 5 Recommendations for Car Dealers looking for ways to stop auto loan fraud.

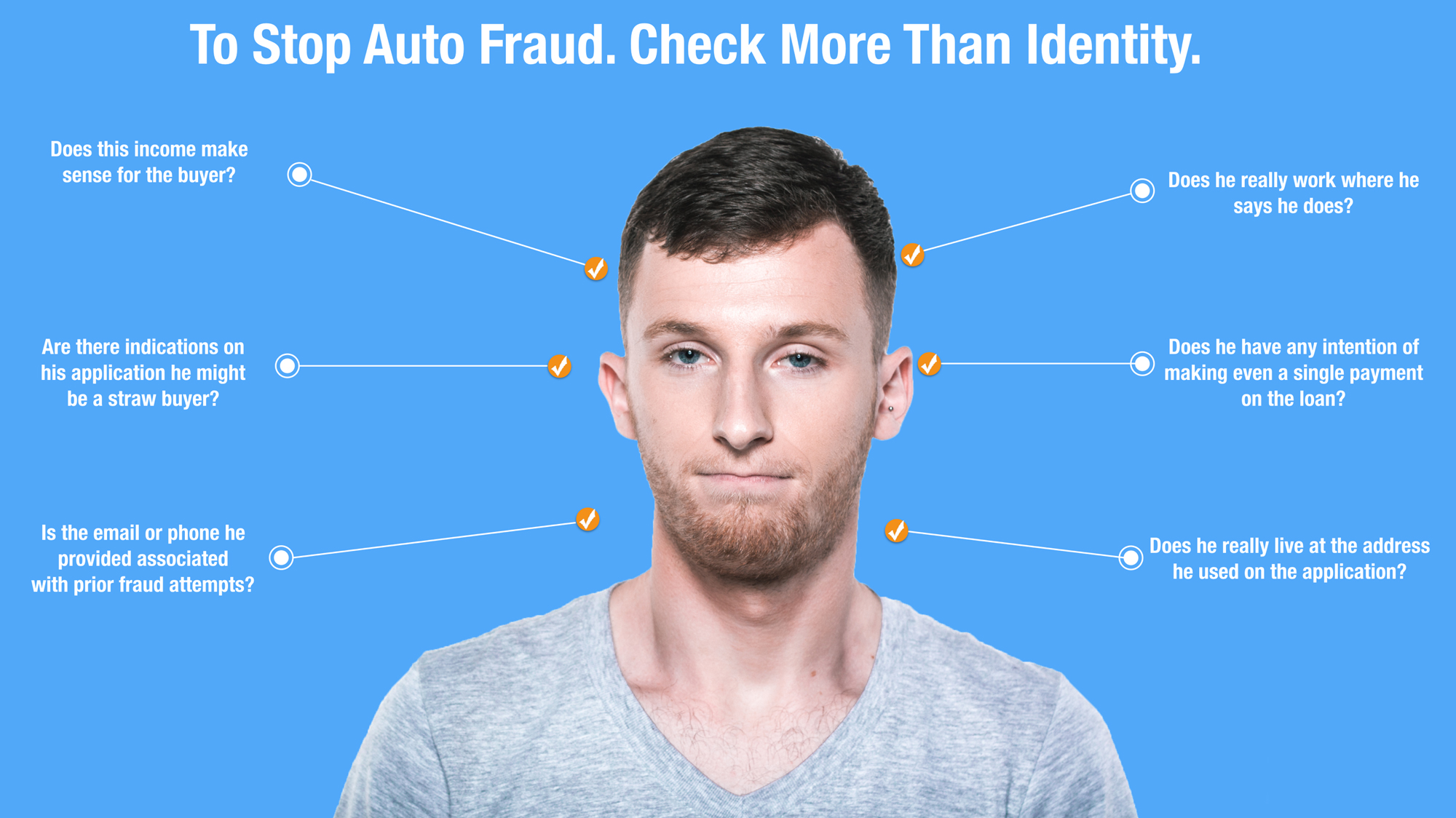

#1 – Don’t Think By Checking ID Only That You Have Stopped Fraud

Only about 15% of auto loan fraud is identity theft. So if your only fraud control is checking a car buyers drivers license or social security card, then you are really only addressing a small fraction of the risk.

There are many types of risk beyond identity theft that dealers need to be aware of.

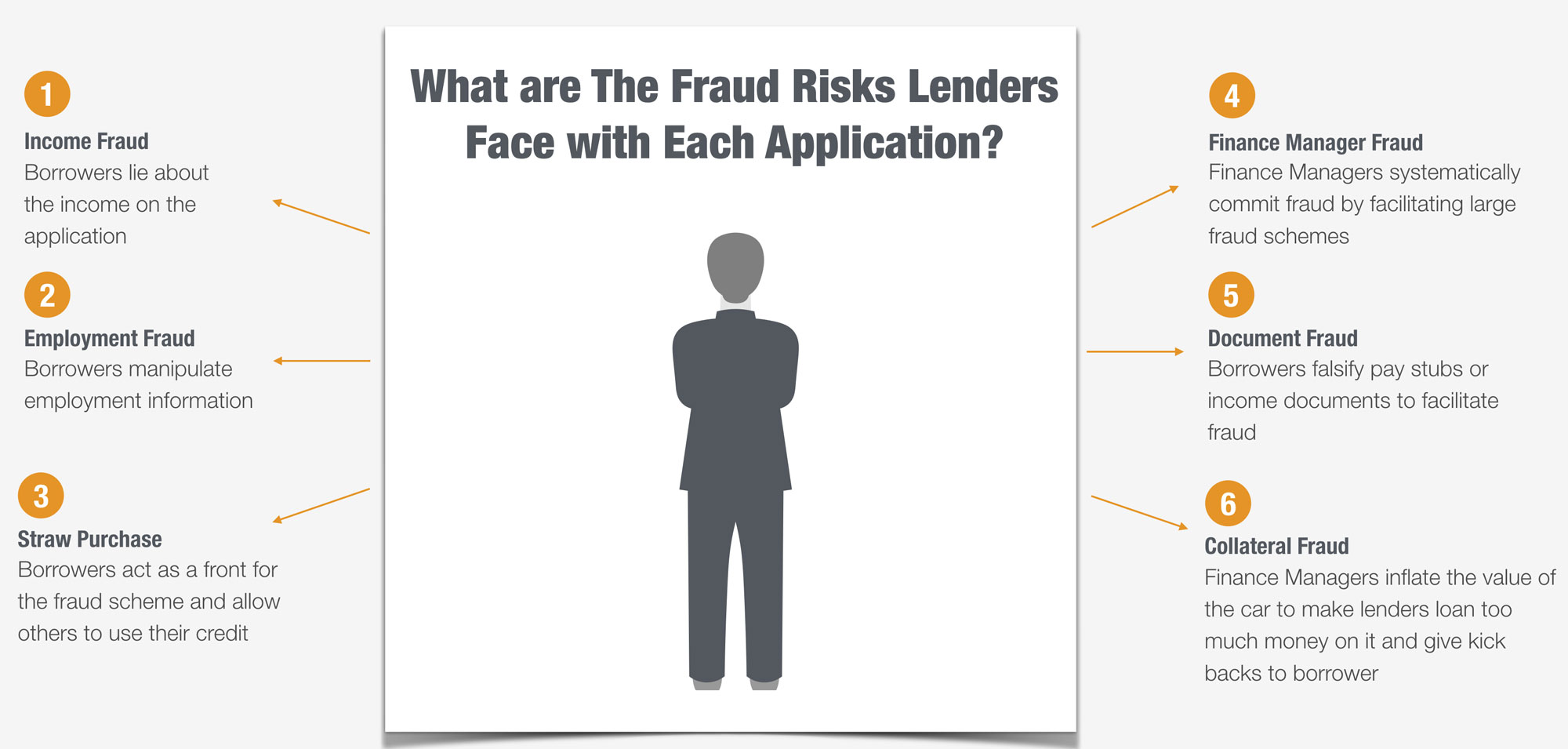

- Income fraud – borrowers lie about their income

- Employment fraud – borrowers lie about where they work, how long they have worked their or job title.

- Straw Borrower Fraud – borrowers or finance managers bring in a person to get the loan who is not the real buyer of the vehicle

- Finance Manager Fraud– unscrupulous finance managers systematically commit fraud or help fraud rings get loans on luxury cars.

- Document Fraud – Borrowers falsify their payment stubs to substantiate their fraudulent income claims.

- Collateral Fraud – Finance managers or sales people load the car up with non-existent add on’s to boost the vehicle value to get a higher loan.

Car dealers should educate themselves on all of these different schemes and be aware that fraud can happen in multiple different ways, not just identity fraud.

#2 – Check if the Income Makes Sense for the Borrower

Income fraud is the most common type of auto fraud and borrowers may lie about their income to qualify for a car that they cannot really afford or to get a better interest rate. Look for red flags of potential income fraud:

- Borrower job does not match income – They say that they work at McDonald’s and make $20,000 a month.

- Borrower income does not match age and experience – The borrower is 19 years old and says that they make $25,000 a month. It could be but isn’t likely.

- Borrower trade-in, car purchase, credit bureau don’t match income – They are trading in a junker, buying a top of the line Mercedes ,they have one tradeline on their credit bureau and they say they make $30k a month. Again it could be but the profile may not match that of a typical high net worth individual who probably has more extensive history.

#3 – Check Employment Discrepancies

Fake pay stubs and borrowers that lie about their employment is a very big deal for auto lenders. In fact, it is quite common for employment information to be fabricated during the auto lending process.

If you want to read up on the proliferation of fake paystub sites on the internet you can read my article here – Fake Paystub Sites, How to Pretend You are Rich.

There are 3 things you can do if you suspect fake paystubs

The fake pay stubs are being used to commit all types of personal, mortgage and auto lending fraud. But the remedy is actually quite simple. And there are 3 big options that I recommend for Auto Lenders.

- Do simple math on the deductions. Almost all of these fake pay stubs will have inconsistent or anomalies with the deductions. Do some simple math based on the states and you will find the fraud in less than 60 seconds.

- Confirm with 4506T – Are you suspicious of the borrower’s income – get them to sign a 4506T and go right to the IRS to verify the income they reported last year. This is far more accurate than a paystub.

- Get their Bank Statements – Check the paystubs against their bank statement deposits to look for inconsistencies.

#4 – Beware of Straw Borrowers

Straw Borrower fraud in auto lending is a growing problem. A straw borrower is a term for an individual whose name, social security number, and credit history are used to hide the identity of the organizers of a for-profit auto or mortgage fraud loan scheme. Sometimes it is a fraud ring, but sometimes it is a shady borrower looking to pull a fast one.

There are some red flags you can look for to stop straw borrower fraud.

#1 Red Flag – The Borrower Profile Does Not Match the Purchase

The first thing to look at is the profile of the borrower vs the purchase and the application itself. Since straw borrowers are not making the purchase for themselves, what they buy does not make sense for them. For example, an 80 year old female buying a turbocharged Mustang with racing wheels and an upgraded stereo might be a straw borrower.

#2 Red Flag – Income and Employment is Inflated

Since straw borrower scams are often fabricated deals, you will often see other indicators on the application that do not make sense. In most cases the income and employment details of straw borrowers are often fabricated as well to make the deal go through. If you put the pieces together you will find the fraud.

#3 Red Flag – Inflated Collateral Value

The most common element of straw borrower schemes is the inflation of the collateral itself. Homes and cars are often inflated so the dealer or the realtor can make a huge profit to make sure they can pay everyone in the deal their kickbacks. Someone has got to pay the bills right.

#5 – Monitor Your Finance Managers

Unscrupulous finance managers can wreak havoc on an otherwise reputable car dealership. Bad finance manager can commit systematic fraud against dealers and cause the dealers to lose their relationships with their lenders. It is important to monitor your dealers to make sure that they are not involved in any shenanigans.

If a finance managers performance is “too good to be true”, it just might not be true. If they can work miracles and get even the most down and out borrower a good quality loan, they might be doing something “extra” to get those loans approved.

Monitor finance managers book of business weekly. Look for unusual trends or spikes in volume. Look for a rash of atypical borrowers buying and getting loans on vehicles in a short period of time with a new finance manager.

These are all sure fire signs that something might be amiss.

To Stop Auto Fraud, Check More Than Identity!

I hope this was helpful. Send me an email if you have any questions! Thanks for reading.