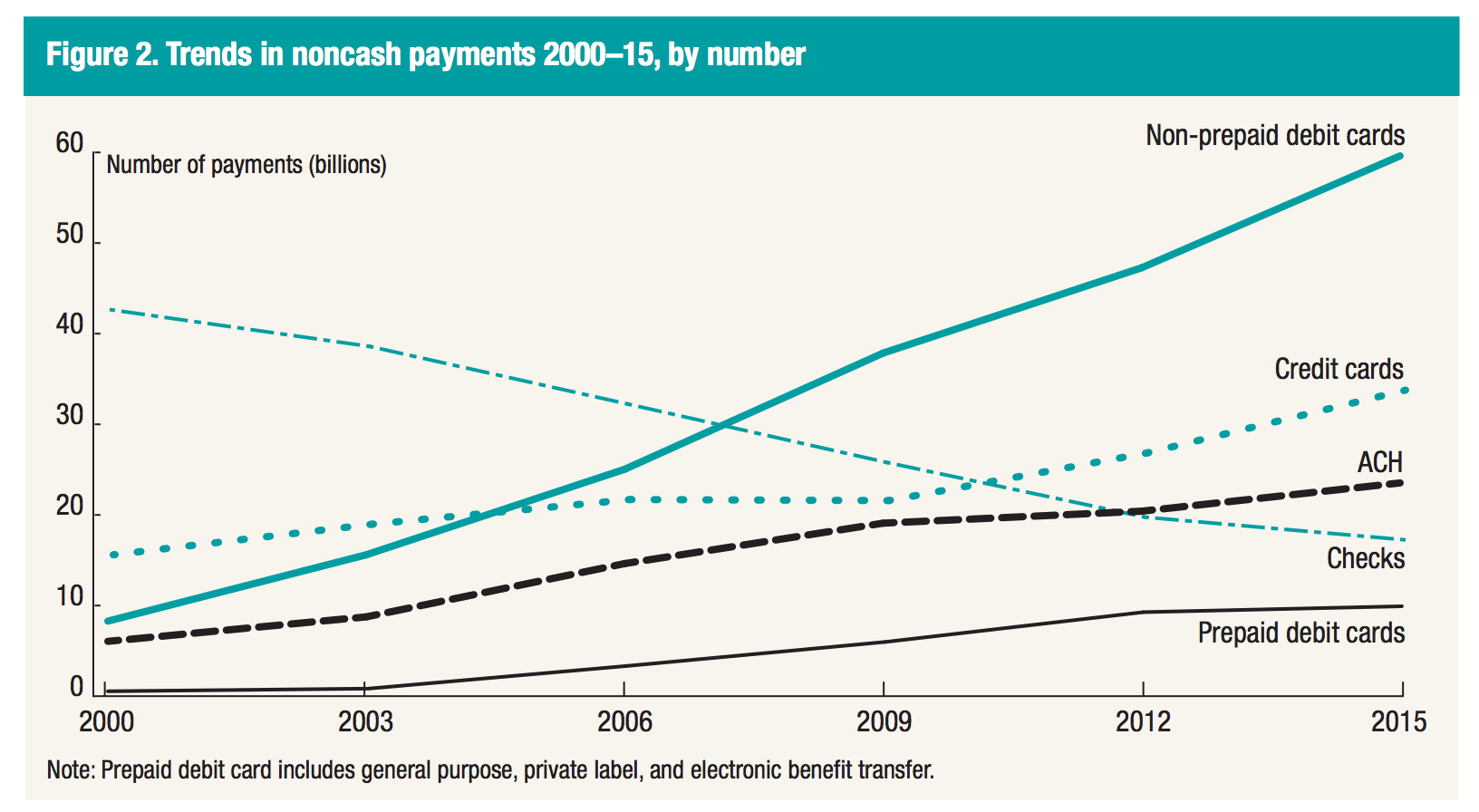

Check use is declining. Each year, use of checks declines about 5% and last year, that number fell to about 17 billion checks here in the US.

By comparison, Americans use their debit cards now about 70 billion times a year – about 4 times as often as they write checks. In fact, Checks are the only non-cash form of payment that is in a free-fall.

With Check use declining, many have assumed check fraud will fall and become negligible. But that hasn’t happened. In fact, annual check fraud losses have been relatively flat over the last 10 years- even while valid check use has tumbled.

Annual Check Fraud Losses

Check fraud still remains one of the highest losses for banks each month. The ABA estimates that approximately $7 Billion in forged, counterfeit and lost and stolen checks were processed through banks in 2015.

In 2003, Check Fraud was estimated to be $5 billion dollars when the number of checks written was over 40 billion – which is over twice the number of checks written last year.

So why has the rate of fraud grown so rapidly in a period when check use has declined so dramatically?

Check fraud losses remain one of the key pain points for banks even has check use declines.

Scams are Fueling Check Fraud, Even While Use Declines

To understand why check fraud has risen, you need to look no further than scams. Scams against Americans have risen dramatically as more people join the digital revolution. If you want to read about the Top Scams you can do that here.

And nothing lets the fraudsters scam consumers better than fake money orders, fake cashiers checks, fake personal checks and fake corporate or business checks. They use checks to scam billions from Americans each year.

Long Float Times Enable Scammers to Take Advantage

Checks can take days to clear a bank. And during that time that it takes a check to settle, scammers can defraud consumers for thousands of dollars.

You see, most of the scams work like this, where scammers con consumers to deposit checks into their accounts and then withdraw money for them.

- Scammer Contacts Consumer with Offer Too Good to Be True – Scammers will contact a consumer with an offer too good to be true. (Big lottery win, a dream job of working from home making thousands of dollars a week, an offer to buy something for a sweet price).

- The Scammer Sends A Check – After the scammer gets the consumer to take the bait, they send a check – often a cashiers check or certified check.

- The Consumer Deposits the Check – The consumer deposits the check into their account and it seemingly clears for them to use (because the scammers keep the amounts low enough that banks often let the checks clear without collecting funds)

- The Scammer Ask for Money Back – The scammer then makes up some complex story of why they need some money back from the check. The consumer sends wire transfers of gift cards to the scammer.

- The Check Bounces – The check inevitably bounces and the consumer is left with thousands of dollars in overdrafts and fines on their checking account.

This scam repeats itself over and over again through a variety of fraud schemes; Ebay buyer scams, Lotto Scams, Secret Shopper Scams, Romance Scams and many others. The proliferation of these scams and growth in their frequency means that we can continue to expect high check fraud losses for many years to come.

Banks Have Not Invested Nearly Enough in Check Fraud Solutions

Year after year check fraud solutions become increasingly antiquated as banks fail to make investments to improve those systems. Banks are hesitant to make investments in an area that they see a limited runway of time. As check use declines, Banks feel that their exposure will reduce over time.

But that is not the case, in fact on a rate basis, check fraud is increasing as check use declines. Fraudsters and scammers take advantage of this failure to invest in modern solutions and bilk consumers and the banks themselves out of billions of dollars.

At some point it will become important to banks to evaluate their check fraud strategies and make investments in new technologies, models and solutions that an help better detect these losses which force millions of consumers to lose money each year.

I hope you enjoyed the article, would love to hear your thoughts.