Don’t cue up the old western music. I’m not talking about actual shotguns here. And I’m not suggesting you buy a gun to protect yourself.

What I am talking about is a very specific type of fraud scam that some in the industry like to refer as “Shotgunning or ShotGun Fraud”. Actually it’s not a fraud per se, rather a technique that fraudsters use to commit a variety of fraud schemes.

By arming yourself, I am suggesting you consider the importance of sharing your fraud data with other banks. Banks that share their fraud data are armed against these types of schemes. Banks that don’t are the victims. It’s that simple.

ShotGun Fraud Can Hurt You

ShotGun Fraud is the technique fraudsters use to rapidly submit fraudulent applications, liar loans, small business loans or even counterfeit checks to multiple banks at the same time in the hopes that banks will simultaneously approve the item.

The scam works because many banking systems and credit bureaus take time to reconcile their systems and post new items. For example, a check may not post to an account immediately rather at midnight of that day so fraudsters could pass that check off to multiple banks or even cash the item at another branch before it is detected.

And credit bureau tradelines will not post to a person’s credit bureau for 30 days giving a fraudster a month to apply for many loans before a bank is notified.

Fraudsters have anywhere from 3 hours to 30 days to carry out a successful ShotGun Fraud Scheme. Fraudster take advantage of slow processing times to steal from banks and lenders.

There are 2 primary ways that criminals use the ShotGun technique to steal from banks.

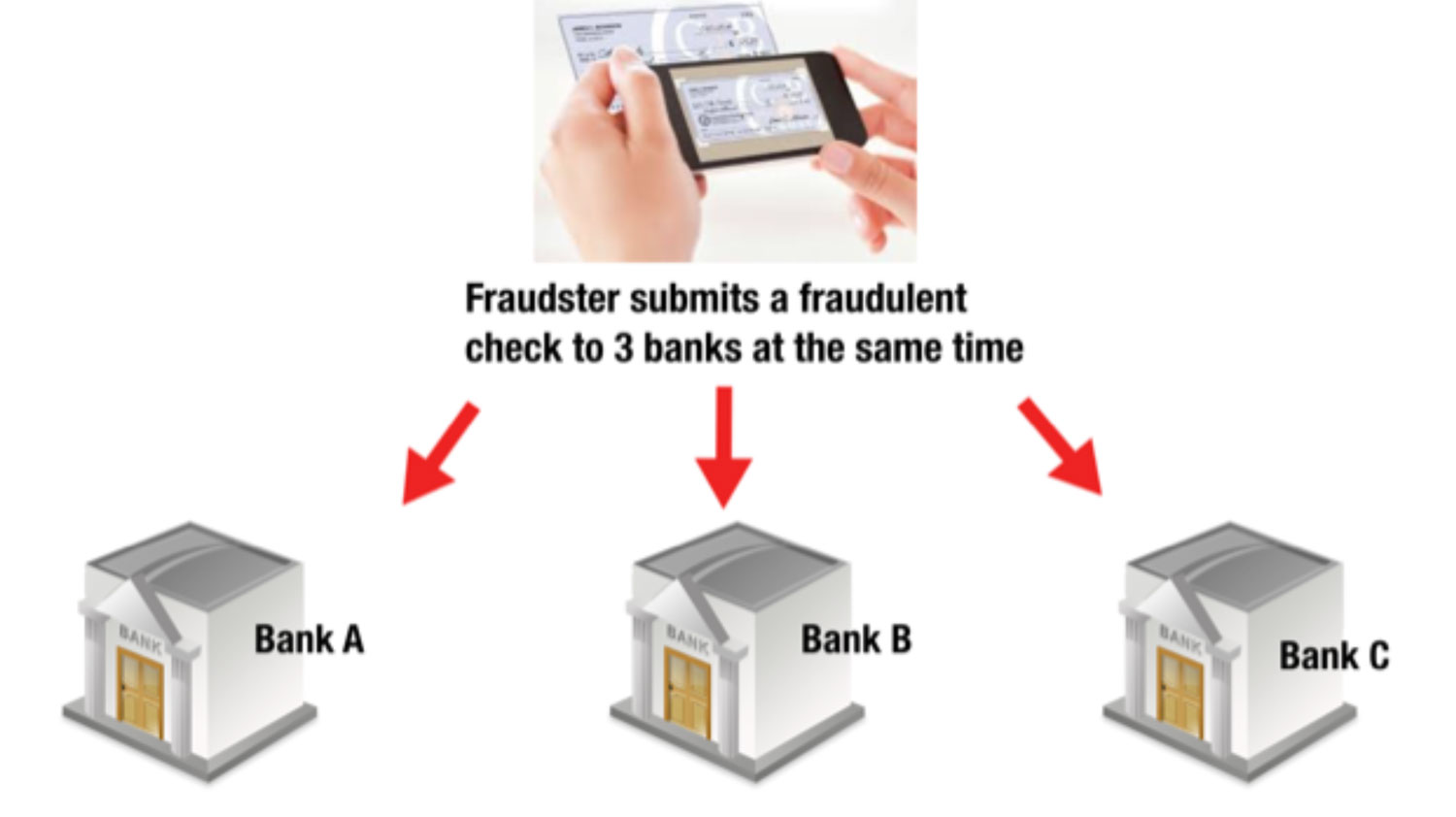

Check ShotGunning – Depositing the same check rapidly to many different banks through their mobile phone since banks may not post the check until Midnight to the account.

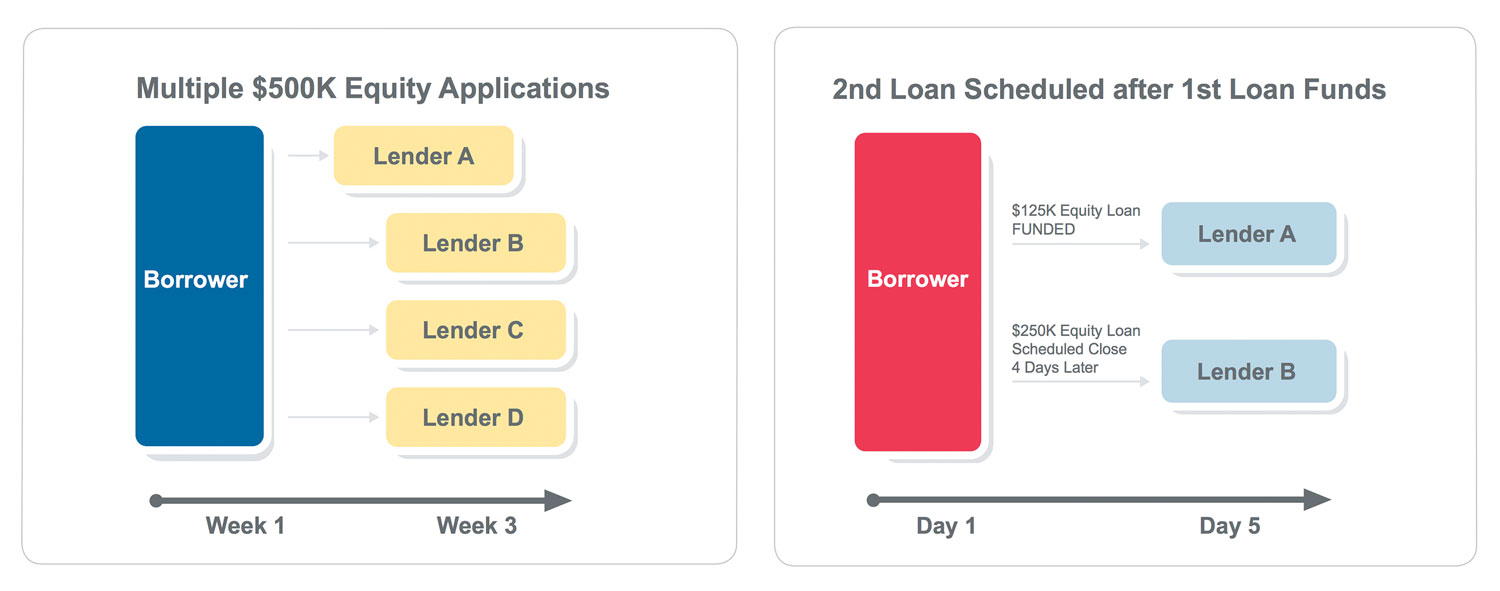

Home Equity ShotGunning– Applying for multiple Home Equity loans from many banks simultaneously to take advantage of the fact that the credit bureau tradeline will not appear for 30 days and banks won’t know the equity in the home has already has a lien against it.

The combined losses from ShotGunning fraud is well over a billion dollars annually here in the United States

Home Equity Loan ShotGunning Emerged in 2004

Home Equity ShotGunning really accelerated in the United States in 2004 at the height of the mortgage boom. Property values were soaring. Millions of homes that were highly leveraged, suddenly had tens and thousands of dollars in equity that could be extracted by borrowers.

The high level of home equity was perfect kindling when combined with the lax lending standards of banks at this time. It was a perfect storm of fraud; lots of eager fraudsters wanting to cash in on new found equity in their home, and greedy banks that were willing to do anything to loan them the money so they could sell the loans off to investors.

Shotgunning emerged when fraudsters realized that Banks and Lenders underwriting processes were ripe to take advantage of. In some cases lenders didn’t even validate that the borrower was the rightful owner of the property and took the borrower’s claim at face value.

In other cases lenders relied on letters from borrowers that the rash of inquiries that appeared on their credit bureaus from other home equity lenders were merely them “shopping around” for the best rates.

CoreLogic a data and analytics company in Orange County was the first company to recognize the problem and educate the industry on the risk associated with this scheme.

Typical Home Equity ShotGun Fraud Flow

When the floodgates of Shotgunning fraud opened it hit the mortgage industry hard with hundreds of millions of fraudulent home equity loans originated.

And lenders were left holding the bag. Since multiple lenders were lending on the same property at the same time some properties had 10-15 separate liens placed on them. Those lender never recouped a penny since the mortgage market tanked, and most homes were underwater.

An individual can easily extract $1 – $2 million on a single $250,000 residence, providing ample incentive to attempt the fraud. CoreLogic

California was the hardest hit as fraud rings in Glendale and San Jose assembled groups of industry insiders including brokers, appraisers and agents that worked in cahoots with straw borrowers to hit the industry for millions of dollars a day in fraud.

The Mortgage Industry Turned to Fraud Consortiums

The only real solution to shotgunning is data sharing. Banks and lenders sharing data with each other to alert other banks when they are receiving applications simultaneously to each other that might cause them both to lose.

So Corelogic created an immensely popular program called the Multi-Closing Alert Program which shut the door on fraudsters almost immediately. The top 9 banks in the country got together and began sharing data with each other on applications that they were about to close and fund. CoreLogic would notify banks when it appeared that other applications for loans were about to close with other lenders.

Lenders could simply pick up the phone and contact the other lender to verify if they were about to close on the same property. It worked beautifully. Shotgunning fraud was eliminated almost entirely by those banks and the fraudster shifted to smaller banks. The consortium grew to most banks in the US until the fraudsters had nowhere else to go.

Fraudsters Shift Their ShotGunning to Mobile Check Deposits in 2011

It’s a good thing for fraudsters that Banks keep coming up with new and innovative ways to make things convenient for customers.

And nothing seems to be more convenient for customers than being able to deposit their checks right from their mobile phones rather than trudging down to the ATM or the Teller window.

According to studies, Mobile Deposits (sometimes called remote deposits) are expected to surpass 1.5 Billion checks in 2016. Proof positive that customer love this service from banks. Mobile Deposit has come along way since USA launched the very first service back in 2009.

In 2011, some banks started seeing fraud creep in on mobile deposits. Since consumers didn’t need to physically pass the check to the bank, rather take a picture of it, the check was able to be deposited multiple times to multiple banks merely by submitting it frequently.

Fraudsters saw this opportunity and quickly moved from Home Equity Shotgunning to Mobile Check Deposit Shotgunning and it was extremely lucrative.

Consumers were the first to notice such as Louise Rosales whose story was told by Bob Sullivan in his article titled “The next fraud wave: When banks cash the same check twice, you might have to pay”

It happened to Louise Moon Rosales of Vermont. Twice in the past year, she wrote checks to pay for small services such as yard work. Both were cashed…and then cashed a second time a few months later. Her bank honored both payments. For example: a $100 check she wrote to a high school student for yard work was cashed in December, and then again in April. How?

The student used a new, popular checking account tool called “remote deposit capture” — he deposited the check with his cell phone. Check recipients who do that get to keep the paper check, rather than hand it over to a teller or an ATM. That means the check can be deposited a second time, a problem known in banking as “double presentment.”

“I totally could have missed it,” Rosales said. “If didn’t use Quicken I would have….I use online Quicken to reconcile the accounts, and that is how I found it.”

Mobile Deposit ShotGunning Fraud Approach $1 Billion in the United States

According to reports, 67% of banks are now experiencing mobile check deposit fraud in 2016. And the growth in Mobile Deposit Fraud Reporting is skyrocketing, approaching 400% in the last year alone as more banks experience this fraud more often.

ShotGunning, the most popular form of Mobile Deposit Check Fraud is one of the largest reported fraud types is estimated to be a whopping $864 Million in Annualized Losses.

Fraud Consortiums Come to the Rescue Again

To solve the problem, banks turned to lessons learned from other industries on how to solve fraud – data sharing.

Two companies lead the charge to fill the need EWS and Fiserv. Each of these companies offered a solution which allowed banks to share information on checks that were deposited with each other anonymously. If it looks like the same check was deposited in another institution, banks could be alerted in realtime when the deposit was being made.

While these solutions are receiving rapid adoption, the fraudsters are quickly adapting their behavior as they did with mortgage lending and are attacking banks that are not sharing their data since they are the weakest link.

Online Lenders Are Now Battling the Same Problem

In 2016, Online Lenders began to notice the problem of ShotGun Fraud from many small businesses. The practice which is called “Loan Stacking” occurs when multiple lenders make the same loan to borrowers in a short period of time without understanding the borrower’s increasing debt obligations and deteriorating credit quality.

As Online Lenders race to get more business, they are using algorithms that can help speed up the underwriting process. Fraudster have figured which credit bureaus the lenders use and they know that information between the credit bureaus may be different. By carefully timing and submitting loans to various online lenders simultaneously, borrowers can manipulate the lenders into lending far more than the borrower qualifies for.

Fraudsters will Never Stop, So You Shouldn’t Either

I think the case of shotgunning fraud is a prime example of why you need to constantly evolve strategies and constantly invest in new tools while relying on data sharing and fraud consortiums.

Fraudsters quickly learned that mortgage lenders were actively sharing data to stop Home Equity Shotgunning and quickly moved to Mobile Check Deposits.

So what’s next? We know the fraudsters are already scheming their next play. So what do you think it is.

I’d love to hear from you.

158 comments On Don’t Get Hit with ShotGunning Fraud

If some one needs to be updated with latest technologies afterward he

must be visit this site and be up to date daily.

corado.shop

Hello, I think your blog might be having browser compatibility issues.

When I look at your blog site in Ie, it looks fine but when opening in Internet Explorer, it

has some overlapping. I just wanted to give you a quick heads up!

Other then that, superb blog! I saw similar here: e-commerce and also here:

sklep internetowy

Good day! I know this is somewhat off topic but I was wondering which blog platform

are you using for this website? I’m getting fed up of WordPress because I’ve had problems

with hackers and I’m looking at options for another platform.

I would be fantastic if you could point me in the

direction of a good platform. I saw similar here: ecommerce and also here:

sklep

I all the time used to study piece of writing in news papers but now as I am a user of net so

from now I am using net for posts, thanks to web.

I saw similar here: sklep and also here: dobry sklep

Great post but I was wondering if you could write a litte more

on this subject? I’d be very thankful if you could elaborate a little bit more.

Thanks! I saw similar here: Sklep and also here: sklep internetowy

Wow, awesome weblog layout! How lengthy have you ever been blogging for?

you made running a blog look easy. The full look of your

site is great, as well as the content material! You can see similar:

https://fordero.shop and here Fordero.shop

Wow, superb blog format! How long have you ever been running a

blog for? you made blogging look easy. The entire glance of your site is fantastic, as smartly as

the content material! You can see similar: dobry sklep and here ecommerce

Incredible points. Great arguments. Keep up the

great effort. I saw similar here: e-commerce and also here: sklep internetowy

It’s actually very complex in this active life to listen news on Television, therefore I

just use the web for that purpose, and obtain the

hottest information. I saw similar here: sklep internetowy and also here: najlepszy sklep

Woah! I’m really digging the template/theme of this blog.

It’s simple, yet effective. A lot of times it’s hard

to get that “perfect balance” between superb usability and visual

appearance. I must say you’ve done a amazing

job with this. Also, the blog loads super quick for me on Chrome.

Superb Blog! I saw similar here: dobry sklep and

also here: dobry sklep

Aw, this was a very good post. Taking the time

and actual effort to make a really good article… but what

can I say… I procrastinate a lot and don’t manage to get nearly anything done.

I saw similar here: najlepszy sklep and also here: ecommerce

Hi, i think that i saw you visited my website thus i came to “return the favor”.I am trying to find things to enhance my site!I suppose its ok

to use some of your ideas!!!

It’s very interesting! If you need help, look here: hitman agency

Great blog here! Also your site loads up fast!

What host are you using? Can I get your affiliate link to your host?

I wish my web site loaded up as quickly as yours lol

I saw similar here: Ecommerce and also here: sklep Internetowy

Hi, I do believe this is a great website.

I stumbledupon it 😉 I’m going to revisit yet again since I book-marked it.

Money and freedom is the greatest way to change,

may you be rich and continue to guide others. I saw similar here: sklep and also here: sklep

internetowy

https://hitech24.pro/

https://gruzchikivesy.ru/

https://gruzchikimeshki.ru/

https://gruzchikinochnoj.ru/

https://gruzchikiklub.ru/

https://gruzchikiperevozchik.ru/

https://gruzchikikar.ru/

https://gruzchikigastarbajter.ru/

https://gruzchikiperenosit.ru/

https://gruzchikiestakada.ru/

https://gruzchikimore.ru/

https://gruzchikiustalost.ru/

https://gruzchikikuzov.ru/

https://gruzchikiperevozka.ru/

https://kupitzhilie.ru/

https://arcmetal.ru/

https://spbflatkupit.ru/

https://spbdomkupit.ru/

https://spbkupitzhilie.ru/

https://ekbflatkupit.ru/

https://zhksaleflat.ru/

https://vsegda-pomnim.com/

http://klublady.ru/

http://diplombiolog.ru/

http://diplombuhgalter.ru/

https://kursovyebuhgalter.ru

Woah! I’m really enjoying the template/theme of this blog.

It’s simple, yet effective. A lot of times it’s challenging to get that

“perfect balance” between superb usability and visual appeal.

I must say you have done a very good job with

this. Also, the blog loads very fast for me on Safari.

Superb Blog! I saw similar here: Ecommerce

крипто биржи топ

https://zadachbiolog.ru/

https://t.me/crypto_signals_binance_pump/24498/ Standard Price for VIP- membership for 1 Week VIP Membership is 0.0014 BTC, You will do send payment to BTC address 1KEY1iKrdLQCUMFMeK4FEZXiedDris7uGd Discounted price may be different from 0.00075 to 0.00138 BTC, that is why follow to all announces published in our Public channel!

https://zadachbuhgalter.ru

https://otchetbiolog.ru/

https://otchetbuhgalter.ru/

https://resheniezadachfizika.ru/

https://kursovyemarketing.ru/

Услуга демонтажа старых частных домов и профессионального вывоза мусора в Москве и Московской области от нашей компании. Мы осуществляем свою деятельность в указанном регионе и предлагаем услугу разборка фундаментов по доступным ценам. Наши специалисты гарантируют выполнение работ в течение 24 часов после оформления заказа.

Услуга по демонтажу старых домов и вывозу мусора в Москве и МО. Компания предоставляет услуги по демонтажу старых зданий и вывозу мусора на территории Москвы и Московской области. Услуга снос дачного дома с вывозом цена выполняется опытными специалистами в течение 24 часов после оформления заказа. Перед началом работ наш специалист бесплатно выезжает на объект для оценки объема работ и консультации.

Услуга демонтажа старых частных домов и вывоза мусора в Москве и Подмосковье. Наша компания предлагает услуги по демонтажу старых частных домов и вывозу мусора в Москве и Московской области. Наши специалисты бесплатно выезжают на объект для консультации и оценки объема работ. Мы предлагаем услугу снести дом цена по доступным ценам и гарантируем качественное выполнение всех работ.

Услуга демонтажа старых частных домов и вывоза мусора в Москве и Подмосковье от нашей компании. Мы предлагаем демонтаж и вывоз мусора в указанном регионе по доступным ценам. Наша команда https://hoteltramontano.ru гарантирует выполнение услуги в течение 24 часов после заказа. Мы бесплатно оцениваем объект и консультируем клиентов. Узнать подробности и рассчитать стоимость можно по телефону или на нашем сайте.

Hi there! Do you know if they make any plugins to assist with Search Engine Optimization? I’m

trying to get my blog to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Thanks! You can read similar blog

here: Sklep online

оборотень сериал смотреть

It’s very interesting! If you need help, look here: ARA Agency

Лучшие картинки различных тематик https://stilno.site

https://pro-dachnikov.com

https://game24.space/

https://podacha-blud.com/

https://gruzchikirabotnik.ru/

Ищете профессиональных грузчиков, которые справятся с любыми задачами быстро и качественно? Наши специалисты обеспечат аккуратную погрузку, транспортировку и разгрузку вашего имущества. Мы гарантируем https://gruzchikinesti.ru, внимательное отношение к каждой детали и доступные цены на все виды работ.

сколько стоят грузчики в самаре

грузчики недорогие

грузчики Екатеринбург

грузчики услуги

https://gruzchikibaza.ru

https://potreb-prava.com/

https://o-okkultizme.com

https://catherineasquithgallery.com

https://gruzchikikorob.ru

грузчики заказать

Hey there! Do you know if they make any plugins to assist with SEO?

I’m trying to get my blog to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Cheers! You can read similar text here:

Sklep online

Предлагаем слуги: https://lit9.ru, демонтаж фундамента, слом домов.

https://acook.space/

Услуги грузчиков https://mhpereezd.ru с гарантией!

https://mhpereezd.ru

https://gruzchikikorob.ru

https://gruzchikivrn.ru

Hi! This is my first comment here so I just wanted to give a quick shout out

and tell you I really enjoy reading your posts.

Can you suggest any other blogs/websites/forums that deal with the same topics?

Appreciate it!

https://gruzchikivrn.ru/

Do you mind if I quote a few of your posts as long as I provide credit and

sources back to your site? My website is in the exact same area of interest as yours and my visitors

would definitely benefit from a lot of the information you present here.

Please let me know if this alright with you. Cheers!

https://diplom-sdan.ru/

https://diplomnash.ru/

https://kursovaya-student.ru/

https://breaking-bad-serial.online/

https://kursovaya-study.ru/

https://kvartiruise.ru/

https://kvartiruless.ru/

https://kupikvartiruor.ru/

This article has been an absolute gem! Thanks a ton for bringing it to my attention.

This article has been an absolute gem! Thanks a ton for bringing it to my attention.

https://kvartiruyze.ru/

https://kvartirulyspb.ru/

отели сочи с бассейном

сочи гостиницы

https://kvartiruerspb.ru/

https://zhkstroyspb.ru/

May I simply just say what a comfort to discover someone that really knows what they are talking about on the net.

You definitely understand how to bring a problem

to light and make it important. More people ought to look at this and understand this side of the story.

It’s surprising you are not more popular given that you certainly possess the gift.

https://zhkstroykaspb.ru/

https://kvartiruekb.ru/

https://zhknoviydom.ru/

https://zhkkvartiradom.ru/

https://zhknoviystroi.ru/

https://noviydomstroika.ru/

https://diplomsdayu.ru/

https://reshaitzadachi.ru/

https://reshauzadachi.ru/

https://t.me/s/SecureIyContactingClAbot

https://t.me/SecureIyContactingClAbot

https://kursovajaskill.ru

http://womangu.ru

Услуга по сносу старых домов и вывозу мусора в Москве и Московской области. Мы предоставляем услуги по сносу старых зданий и удалению мусора на территории Москвы и Подмосковья. Услуга демонтаж ленточного фундамента выполняется опытными специалистами в течение 24 часов после оформления заказа. Перед началом работ наш эксперт бесплатно приезжает на объект для оценки объёма работ и консультации. Чтобы получить дополнительную информацию и рассчитать стоимость услуг, свяжитесь с нами по телефону или оставьте заявку на сайте компании.

Услуга по сносу старых домов и вывозу мусора в Москве и Московской области. Мы предоставляем услуги по сносу старых зданий и удалению мусора на территории Москвы и Подмосковья. Услуга снос дачного дома с вывозом цена выполняется опытными специалистами в течение 24 часов после оформления заказа. Перед началом работ наш эксперт бесплатно приезжает на объект для оценки объёма работ и консультации. Чтобы получить дополнительную информацию и рассчитать стоимость услуг, свяжитесь с нами по телефону или оставьте заявку на сайте компании.

Услуга по сносу старых домов и утилизации мусора в Москве и Московской области. Мы предлагаем услуги по сносу старых построек и удалению отходов на территории Москвы и Московской области. Услуга http://demontazh-doma-msk6.ru/ предоставляется опытными специалистами в течение 24 часов после оформления заказа. Перед началом работ наш эксперт бесплатно посещает объект для определения объёма работ и предоставления консультаций. Чтобы получить дополнительную информацию и рассчитать стоимость услуг, свяжитесь с нами по телефону или оставьте заявку на веб-сайте компании.

Услуга по сносу старых зданий и утилизации отходов в Москве и Московской области. Мы предоставляем услуги по сносу старых сооружений и удалению мусора на территории Москвы и Московской области. Услуга http://demontazh-doma-msk8.ru выполняется квалифицированными специалистами в течение 24 часов после оформления заказа. Перед началом работ наш эксперт бесплатно посещает объект для определения объёма работ и предоставления консультаций. Чтобы получить дополнительную информацию и рассчитать стоимость услуг, свяжитесь с нами по телефону или оставьте заявку на сайте компании.

Услуга по сносу старых зданий и утилизации отходов в Москве и Московской области. Мы предоставляем услуги по сносу старых сооружений и удалению мусора на территории Москвы и Московской области. Услуга демонтаж домов в московской области выполняется квалифицированными специалистами в течение 24 часов после оформления заказа. Перед началом работ наш эксперт бесплатно посещает объект для определения объёма работ и предоставления консультаций. Чтобы получить дополнительную информацию и рассчитать стоимость услуг, свяжитесь с нами по телефону или оставьте заявку на сайте компании.

https://kursovuyupishem.ru/

Каталог салонов эпиляции https://findepil.ru/ Москвы и Московской области. Химки, Люберцы, Красногорск, Зеленоград и т.д. Все виды эпиляции – электроэпиляция, депиляция воском, шугаринг, лазерная эпиляция. Можно выбрать салон по цене, для примера выбраны стандартные процедуры эпиляции – руки воск, ноги шугаринг. Каталог постоянно пополняется.