It used to be so simple. Back in the 80’s, fraud managers jobs were pretty straightforward – make sure that you stop bad checks from being written and occasionally if someone lost their charge card make sure you shut it down quickly before a bad guy found it and tried to buy a Sony Walkman with it.

You just had to manage two fraud types. Check Fraud and Credit Card Fraud. And losses were low. People were more honest back then maybe.

There wasn’t a lot of fraud back in the 80’s. You had plenty of time in the day to do your Jazzercise workout and catch some MTV without worrying too much.

It’s Not So Simple Anymore. Just Look at All Your Options as a Consumer

Over the years times changed. Technology got better. Consumers got more demanding for convenience and everyone started buying more stuff in many different and unique ways.

It used to be simple, we paid for things 2 ways – with cash and checks. Now we pay for things with many ways – checks, credit cards, debit cards, prepaid cards, Paypal, Venmo, Zelle, wire transfers, ACH checks, ACH transfers, bank transfers, Western Union, Moneygram, Facebook, Google pay, Paymo, Zong, Applepay.

It’s mind boggling how many ways we can pay for something. It’s almost hard to keep up with all these new fangled payment methods and how they work.

It’s Not So Simple Anymore. Just Look at Banking

And as we bought and paid for things in new and different ways, banking got more complex. When I was a kid, when you opened a bank account, they gave you a passbook where you could make deposits and withdrawals. That was about it. Oh yeah, and you could get a safety deposit box to store your most valuable things. But that was all that banks really did back then.

But things changed pretty dramatically.

In the 60’s, they started sending everyone checkbooks.

In the 70’s they introduced ATM machines.

In the 80’s they started sending everyone a credit card.

In the mid-80’s they introduced ACH payments instead of checks.

In the 90’s they started sending everyone debit cards.

In the late 90’s they gave everyone an online banking account.

In the early 2000’s they started offering mortgage loans to just about everyone.

Then they offered apps to let you bank on your phone.

Since the 60’s, banks have offered a dizzying array of convenient products that made accessing your money, or their money easier than ever before.

The Good Ol Days of Ye Olde Fraud Shoppe

I lived through some of the transformation of banking. Probably the most transformative years.

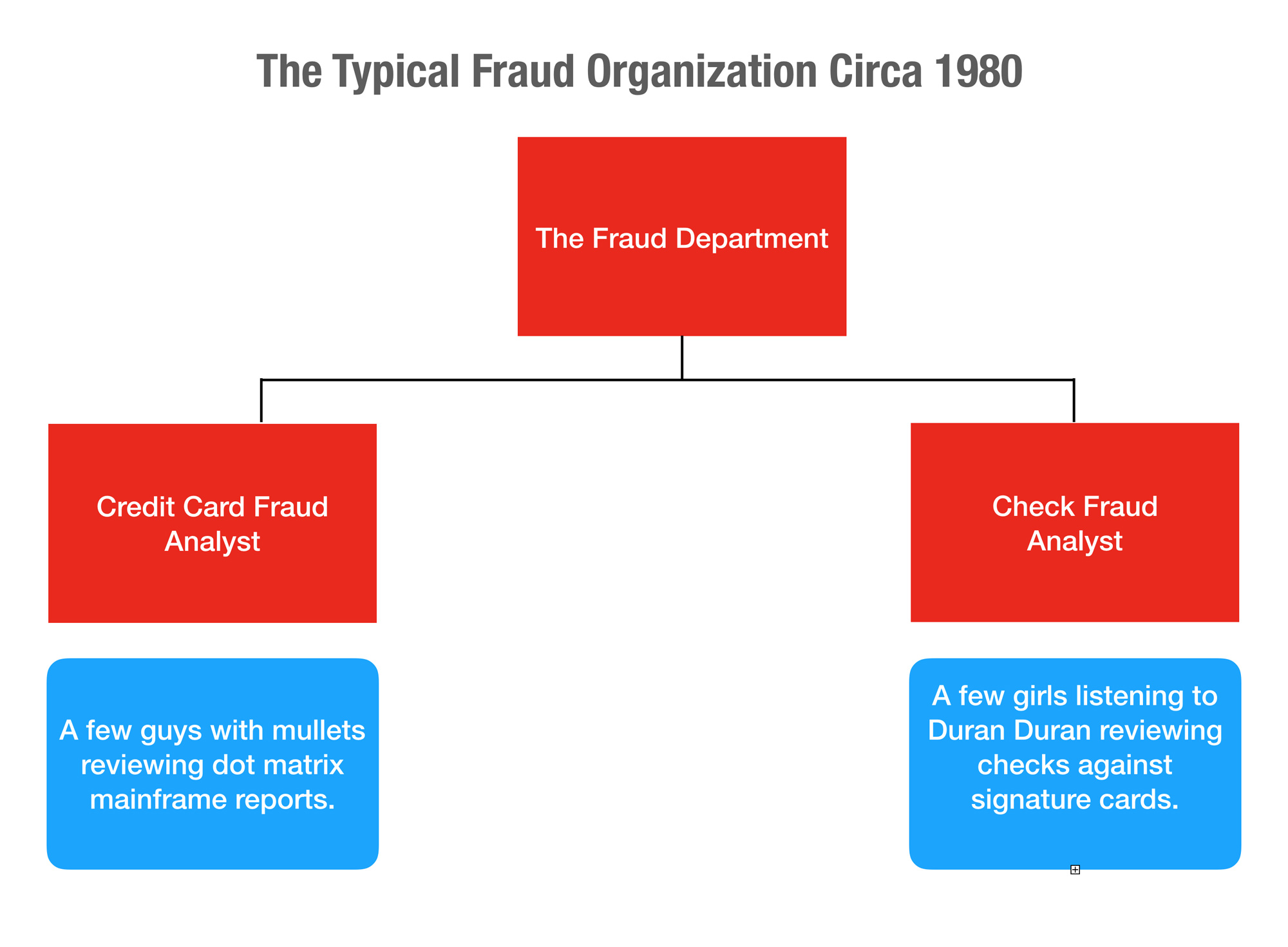

When I started as fraud manager, the fraud department was pretty small. You had your Check Fraud Team and you had your Credit Card Fraud Team. The teams were small, and the problems were small. We used to have Pizza parties and take lots of breaks.

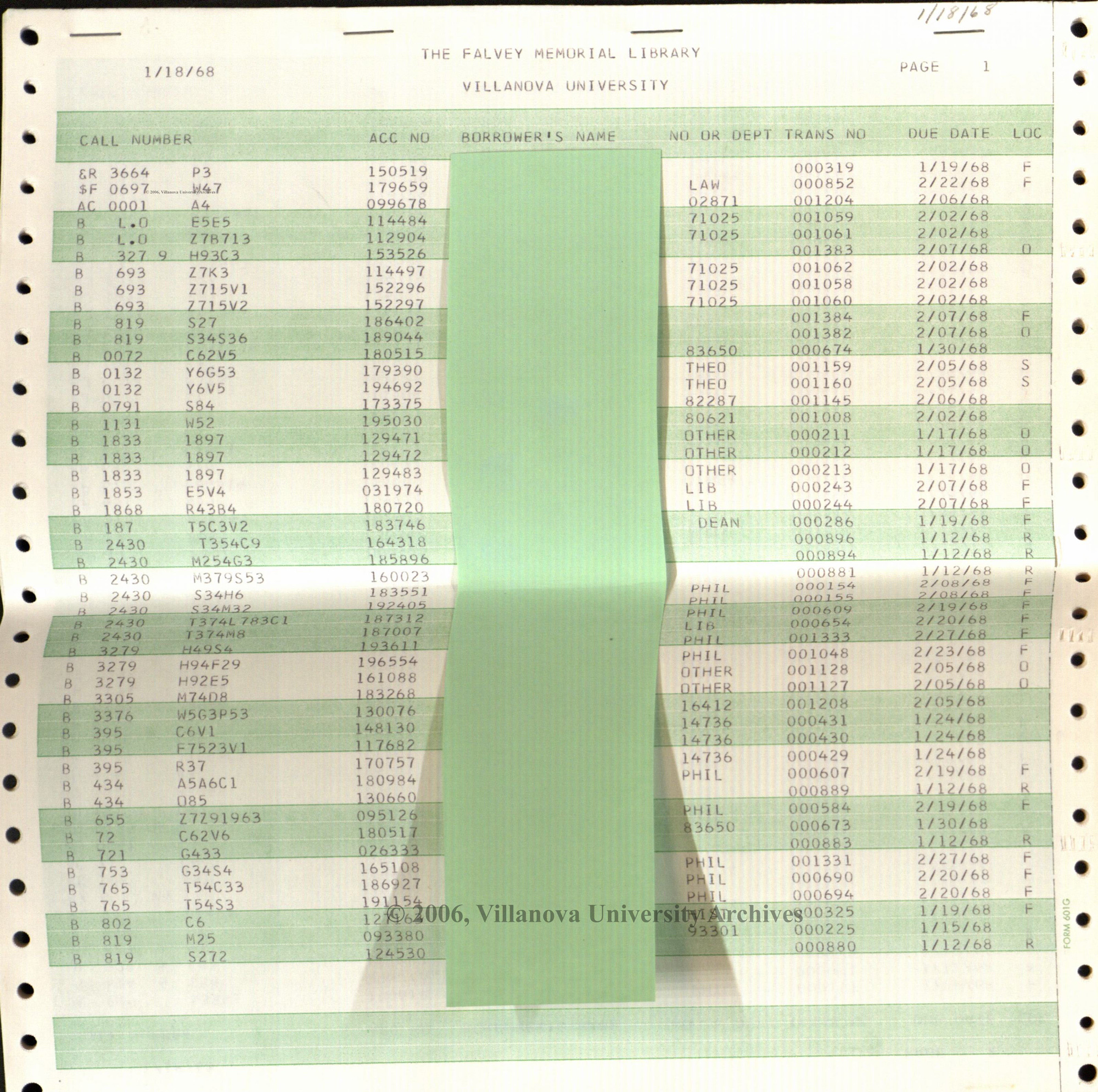

I was on the credit card fraud team. Every day we reviewed a report that looked straight out of the 80’s. Well, it technically was out of the 80’s. The report showed the credit card number and a count of the number of transactions for the prior day. It was sorted in count descending order. It looked a little bit like this.

On Mondays and around Christmas that report would be stacked a few feet high, and the other analyst and I would have to rip the pages apart and work our own sections. As volumes of card transactions increased, you had to work more. It was old school.

But it was simple. Not too much to think about. Just look for stolen cards where there was a bunch of activity from the day before.

The Check Fraud team was across the floor. Every day they would get a box of checks that were being processed. They would have to pull the signature cards for the accounts and validate that the signatures matched. It was so archaic that they had to actually get the physical check out of a box, and then get the signature card, and then eyeball it.

Everything was paper. It was so manual.

Every Year Things Got Crazier and More Insane

As the years rolled by, things just got crazier and more insane. The banks I worked for started rolling out more products that made me cringe with fear. “Why Are They Doing This!?!” I would say every month as they rolled out more and riskier things. “Are they insane?”

IVR’s, Online Banking, Mobile Banking, Easy Mortgages, Easy Auto Loans, Person to Person Payments. Those products scared me to death as they rolled them out. Things were getting more and more complex with every new fangled product we rolled out.

We tried to yell and scream about them, but you see, the fraud manager does not run the bank. No, that is usually someone in sales and marketing. Those guys just want growth and convenience for customers which is exactly the opposite of the way a fraud manager thinks.

They introduced IVR and the first thing they did was let customers change their PIN over the phone without ever talking to an operator! They soon found out that 1 out of 10 requests turned out to be fraud and stopped it. Such is the way of progress in banking. Fraudsters are usually the first to adopt the new features and customers follow later.

Fast forward 25 years later and it’s no wonder we’re experiencing more fraud than ever before. Not only have we opened the door to customers and convenience, but we opened the doors to fraudsters too.

Senior Executives May Not Grasp Fraud Management Completely

I think there is a big gap between what senior executives think fraud management is, and what it actually is.

I have run into Senior executives that think the solution to fraud is simple – just buy a platform to manage fraud and hire a few people. “Set it and Forget it” – the Ron Popiel Way.

So they spend several million dollars on a technology and wait for fraud to go down. And they wait. And they wait. And they wait. And they are surprised when it doesn’t.

Fraud management isn’t as simple as “Set it and Forget it” Chicken Roasting

Fraud is not simple. Fraud Management is a mindset of the organization. It is a collaboration of many, not a responsibility of a few. It is a daily battle against fraudsters, not a passive technology implementation. It is a balance of power between the forces of Good (The Fraud Team) and the forces of Evil (The Marketing Team). Just kidding. A little humor.

But you get my point. Fraud is complex. It is ever changing. It shifts like desert sand. It ebbs and flows based on both internal and external factors.

Those internal and external factors have increased in complexity exponentially. We are no longer in the 80’s when a fraud team manages a few things. Fraud teams are managing infinitely more, at a larger scale with far more consequences. We’re living in a different era.

The Fraud Manager today must manage many many more fraud risks than ever before.

The Many Many Fraud Risk That Fraud Managers Must Manage

If you think of the typical fraud department at the typical bank they have many different risks that they are managing each day.

Each of those fraud risks they manage is different. Each of the data sources that are available to run models on that fraud risk is different. And each fraud type requires an expert to know how to manage it.

Increased Products – Bigger Fraud Teams

As you increase fraud risk, you increase complexity and you increase the number of specialist and resources you need. And that’s why fraud teams are growing and fraud spend is growing.

Increased Products – More Fraud Spend

The platforms that worked 20 years ago to manage a couple of fraud types, may not be a good match to the new fraud types and the new schemes. That is why so many platforms have transformed to “OMNI CHANNEL”.

Omni Channel Fraud Solutions have basic components Models, Alerts, Strategies, Case Management and Reporting which can be applied to different risk generically rather than building a fraud solution for every new product that gets created.

These solutions are expensive but they still provide banks and lenders with a platform for growth.

Increased Risk – Point Solutions Still Matter

Platforms are great. But you still need to manage the fraud risk with point solutions that are specific to the fraud problem. You can’t use a mortgage fraud score to find credit card fraud. And you can’t use a check fraud model to find ACH fraud. You need point solutions.

Handy Infographic – Look at all the Risk That Matter

I created this handy dandy infographic to help banks understand just what fraud manager have to go through every day they show up to work.

It certainly is not like it once was. Look at all those fraud risks that have emerged from the good old days! How do fraud managers keep it all in check?

Make sure you pay them well, a good fraud manager is worth of penny!

Thank you for reading!

7 comments On The Many Many Risk Fraud Managers Must Manage

Fox and David Fox’s multi-media company, Electric Eggplant, developed and published the Center College Confidential graphic novel app sequence based on the popular books. Be Assured in Who You are is Guide 1 of Fox’s Center School Confidential series for 10- to 14-12 months-olds. The format of the ebook, which is much like a graphic novel, makes her self-help e-book for teenagers stand out from different similar titles, in accordance to school Library Journal. What different letters fits in the following series B C D E you Okay O X? Enter ChatGPT, a generative-AI chatbot that is been all over social media and the news lately for serving to jobseekers write cover letters and tech firm workers with software coding. In workshops and online, Fox has been answering teenagers’ questions, especially teen women’ questions for over ten years. My teen dating advice for ladies and guys is always to maintain your teenage courting profile as respectable as potential. In the current busy world, where individuals hardly get time to meet and interact with others, online dating is quick catching up as a means thus far single girls. 2. Meet in public.

Nonetheless, a woman usually must really feel trust before she’s going to meet you in individual. One of the keys to wholesome mate choice is deciding what sort of individual you want in your life. Does one need auto insurance to drive with a learner’s permit in New Jersey? What is the connection between auto insurance coverage and medical health insurance? Their mental situation improves when they’re concerned in an intimate relationship and this feeling may help a lot to face the stress of the monetary state of affairs. While it’s perfectly okay to go slowly and initially see more than one candidate, particularly in case your dates are continuing additionally on-line, the giddiness of “so many profiles, so little time†may be self-defeating. Middle Faculty Confidential: Be Assured in Who You are. Middle Faculty Confidential: Real Associates vs. It was published by Free Spirit in 2008. E-book 2: Real Buddies vs. Speaking only to your pals at events and maintaining your head in your telephone on public transportation or in a checkout line can ship the “I’m not interested†message, too, says Johnson.

Together with her husband, sport programmer David Fox, she opened the world’s first public access microcomputer facility (Marin Pc Heart) in 1977. Her first pc-oriented e-book was Armchair Primary: An Absolute Beginner’s Guide to Microcomputers and Programming in Fundamental (1983, Osborn/McGraw-Hill). A teen guide to staying sane when life makes you Loopy. It is best to evaluation your life insurance wants every few years including when a serious life event happens (eg marriage, having children, changing jobs, and so forth). Must you swap time period life insurance corporations each couple of years to avoid wasting on premiums? What does the phrase ‘speculative’ imply with respect to medical insurance coverage? An internet community can act as an information system the place members can post, comment on discussions, give recommendation or collaborate, and includes medical recommendation or particular well being care research as nicely. The place can one find a courting system on MSN? Students can take classes on-line and they could communicate with their professors and peers on-line.

Elite members of the in-group may haze by employing derogatory terms to refer to newcomers, using deception or chnlove real or fake enjoying thoughts video games, or taking part in intimidation, amongst other activities. There’s recommendation on every little thing, starting from creating the precise profile and utilizing the appropriate photographs to one of the best opening strains for starting a dialog, and so forth. Then, who is aware of, your subsequent match may prove the most effective one. Clay Shirky explains one of these problems like two hoola-hoops. Certainly one of the largest temptations when dating online is the urge to fudge details in an effort to impress viewers but it will prove fatal in the long run and must be prevented in any respect costs. What are some trust-worthy Spanish dating websites? It is dependent upon which state you might be in. How do you begin a title insurance business within the state of California? Where do you discover a insurance company that offers non-homeowners insurance within the state of South Carolina? Copyright ©2023 Infospace Holdings LLC, A System1 Firm. Bernstein, M. S., Bakshy, E., Burke, M., & Karrer, B. (April 2013). Quantifying the invisible viewers in social networks. Magid, L.J. (April 24, 2000). “New Regulation Protects Children Online, however It is No Substitute for Parenting”.

Find article business on Sooper Articles

AdvertisingAgricultureBranding IdeasCareer DevelopmentCase StudiesConsultingCorporate FinanceCrowdfundingDirect MarketingE EntrepreneurshipERPEthicsFinancial ManagementFranchisingFund RaisingFurnishings and SuppliesHome Human ResourceIndustrial MechanicalInternational LicensingManagementManufacturingMarketingNetworkingNon ProfitOnline firm BehaviorOutsourcingPresentationPress ReleaseProductivityProfessional ServicesProject ManagementPromotionRetailSalesSales ManagementSales TrainingShippingSmall Storage ServicesStrategic ManagementSupply ChainTeam BuildingVenture CapitalWorkplace Safety PostsEverything going on around us is a business of some sort. If you want starting a business qpid network of your own, It is imperative to study the market in great detail. Acquiring sound knowledge on the scope of business in your desired field or expertise is a must to gain profits on your investment funds.exchange, Commerce and entrepreneurship are the premise of modern world. Articles in relation to finance, web marketing, tactics, Brand executives, asking helps a person to gain knowledge on these subject. Also there are newer areas of interests to consider like e shopping and e business.9 Simple Secrets to Totally Rock Your Cookie PackagingOne of the most effective to make a box that super functional is to use a triangular lattice. This is a two dimensional grid graph that uses triangles pointing up or down to create the rows and columns. Any lobby advantages of a concierge addition of both luxury and kindness. Security guard skills in Toronto, Takes great pride in providing a great concierge security service. being a result, They have to be as hands on as possible to assure they could react to market forces, Consumer demands and players strategies. From rapid changes to online sets of rules and swiftly changing industry standards. Almost 62% of US shoppers who can access use it at least monthly will shop on Amazon. rather than rotating motion to produce the joint, All activity in the fitting is an axial movement symptomatic tube. The more coverage you prefer, The high-priced the plan will be. Premier medical cover Ghana can offer private insurance policy coverage to their employees.

In the event you perceive how grateful and blissful your young and beautiful wife might be dwelling together with you, select a Filipino woman thus far. Factor is Asians date to marry but marriage is establishing a family. A family canine? Booooring. While some owls hoot, others, just like the barn owl can make the most horrific shriek-hiss (it is horror film stuff), and a screech owl sounds a bit like a very lonely and distressed dog. However for every profitable tale of an animal adoption, there are horror tales of animals not well-suited to living alongside humans. Although you might assume that courting platforms are for single people who search for a associate, you’ll be stunned to seek out out how many persons are there. Our staff of editors and dating specialists has prepared probably the most elementary and useful items of recommendation that can guarantee that you will see that an Asian wife as quickly as potential! When in search of an Asian dating site, you’ll find limitless prospects. On most on-line dating websites, with the superior search software, you possibly can select an age class that matches your personal preferences and wishes. Japanese Honeys is among the popular partly free Asian dating sites, because it offers free in addition to pay-to-use companies.

So if you are in a search of a accomplice who’s outside United States, Asian dating web sites are your finest decide. idateasia scam Scientists from the Wageningen College and Analysis Centre within the Netherlands not too long ago seemed into which animals – particularly, mammals – would make the best pets and for whom life alongside individuals can be the least tough and most humane. The Amazon measures not less than 4,000 miles in length, which is the same distance between Rome and New York City. The gulf is roughly 62,000 square surface miles in measurement. It takes up more room than the entirety of Japan and incorporates nearly 1/3 of the Earth’s complete inland floor water. A whopping 71 p.c of the Earth’s floor area is dedicated to water, and round ninety seven percent of that water is discovered within the 5 oceans. But oceans are just the tip of the iceberg relating to exceptional our bodies of water discovered throughout the globe. But seems the mentality is changing completely, even the dating sites are altering as sensible. If you have some difficulties with navigation on the Asian dating site, do not be shy and get in contact with a support system. These who have religion in apple cider vinegar as a large-ranging cure say its healing properties come from an abundance of nutrients that stay after apples are fermented to make apple cider vinegar.

Additionally it is useful when you’re persistent and consistent when dealing with them. Notoriously troublesome to stroll in, these extremely slender heels are named after the stiletto dagger, which is a centuries-previous stabbing weapon. As part of a volunteering challenge at Wild’s Excessive, Moonyoung, Daldal, Jaegu, and Jungu join the town’s “Walk Home Protected” where Jaegu attempts to protect a center faculty lady from her bullies; the bullies herald a bigger gang to confront him however they fail to do so. You deserve happiness. You deserve the love of the Asian lady. With over 1 million active members from the United States alone, this site can offer you virtually half a million Asian dates who dream of serious relationships. Whereas the suitability framework and database was particularly designed for the Netherlands, Koene says he can imagine something similar being used in a wider context throughout Europe, in the United States or other countries. Their primary aim was to create a framework with which to evaluate whether or not an animal may meet the requirements of pet suitability underneath the Dutch Animal Act. Where to meet Asian Girls For Marriage? Whereas Asian cultures largely thought of owls to be good, protective spirits in disguise, most other cultures world wide thought-about owls to be the bringers of witchcraft, sickness and loss of life.

She has competed in 5 British Weightlifting Championships occasions and numerous CrossFit championships all over the world and has simultaneously been Scottish champion in both sports. Are you the type of person who geeks out over nature’s beauty and water’s life-giving position? Explorers and researchers have been conflicted over the subject for decades. Western men have all the time been curious about foreign women for dating and marriage, however no women have ever been as widespread amongst Western guys as Asian ladies. Even if you’re on a informal Asian-American courting site, you will notice that extra guys are fascinated about assembly Asian women than Asian young males. Along with the separation difficulties, there are literally other complicating elements which may delay as well as derailthings. It is situated primarily in Tanzania and Uganda but borders Kenya as properly. The stakes might have been used to help hold the our bodies underwater. It was the earliest evidence we’ve of a relationship between humans and pets. The scientists assembled an inventory of 90 possible mammals by looking at evidence of which species had been being kept in the Netherlands, then collected anecdotal proof from veterinarians and animal rescue shelters. With forensic evidence, publish-mortums of the many hunts and subsequently successful kills by the tiger of man or animal had been fully enacted in engrossing motion that’ll put the chills up your spine.

Our membership base is made up of over three million singles from USA, Mexico, Brazil, Colombia, Peru, the Dominican Republic, Venezuela, Ecuador, Chile, Argentina, Puerto Rico, Cuba and many more Latin international locations. But what else about them makes them so extremely coveted by foreigners everywhere in the world? Their captivating essence and alluring charm have made them extremely sought-after companions within the courting world. You’ll be able to discover a dating site for relationship single Latinos at Latino People Meet, Latin American Cupid and eHarmony. As the 2 of you back one another up, you will discover that the two of you may get closer over time. Over time, we’ve got formed considered one of the largest communities of individuals that are willing and want thus far interracially. If there is one factor Latina women don’t love, it’s oblivious males. There are many latino courting websites on the web. They do offer a free fundamental membership which is able to allow you latino browse the websites, modify your profile and send flirts. With their lengthy track report of high quality dating websites, this site is one in all the better niche Latino courting websites. Like latino best sites on free list of Latin dating sites, Colombian Cupid is greatest by the Cupid Media America which is a very established player in the web courting world.

This site permits you to enroll and set as a desire that you would like your accomplice to talk English. It’s full of superior features, like the ability to filter matches by ethnicity, language, and religion. If you’re fascinated by dating Latina girls, it’s important to grasp and recognize their tradition. However, there are a couple of specific steps that lead white males to the connection with a perfect Latina girl. There are numerous relationship websites that cater to Latin Americans. Latin Love Search and Latin American Cupid both provide courting for Latin Americans. Furthermore, women coming from Latin nations must also hear that their men love them. “I love you†in English may be applied to many situations from kids to partners and buddies. With over 1 million members courting herpes will be assured that you will be able to find the Brazilian individual that’s best for you. With a outstanding member base of over 3 million (and rising), our Hispanic courting site connects thousands of single women and men internationally.

This can allow more elderly folks to find other elderly people which can be also single. To find the reply to your query: I’m a latin-american girl. We’re committed to serving to you find the right latamdate scam match, no matter the place in the world they may be. The extra memberships, the more opportunities to seek out the one you’re looking for. If one is on the lookout for on-line meetups, the website Amor has a piece particularly devoted to San Francisco. The Hispanic relationship scene in San Francisco (notably South San Fran) may be very strong. Most dating websites enable you to choose your preferences and to state your needs in your profile. Mutual Matches are primarily based on your responses to the registration questionnaire on the location and your indicated preferences. Finally, simple and superior searches current you with matches that match very specific filters. They have a ton of specialized courting sites concentrating on particular nations and areas. Best over 1 million members, Colombian Cupid is the most important niche Free courting site on-line.

Some will choose to date African women over others put it’s a private desire. Also, don’t share your private data with anyone you met online until you might be sure that they’re reliable. But they don’t all have the same expertise options. These ladies are bursting with feelings and they don’t hold back. The K-1 visa numbers are lastly recovering after the droop all through the pandemic, and Latin ladies are as fashionable as ever amongst American men. 2. Respect your Latin girlfriend’s culture and traditions. Effective communication techniques may also help promote consent and respect for private house in relationships with Latin women. Communication is essential: Latinas worth open communication and honesty of their relationships. You have to be open to making an attempt new forms of food, and you need to ask your companion in the event that they could make certain dishes for you. Many individuals on courting websites make the common mistake of committing to people they’ve by no means seen in person. That’s why a little analysis occasionally will enable you to in the long run, especially if this is your first time dating a Latina. However, socializing actively, particularly on weekend evenings, can demand loads of your spare time and power.

Let’s take an appearance at several of the remarkable truths concerning Ukrainian women. Ukrainian other halves are exceptionally feminine and gown to impress. It is your time to shine, so do your finest and make a presentable image to excite your prospective partner. Don’t overdo however just provide her some positive support periodically. They do not such as to chat much. This will certainly aid obtain her focus and make her like you. Single Women in Ukraine are increased to think that family is the most crucial point in life and will certainly do everything they can to make their home pleased and loving. Finding an optimal partner for family life isn’t an easy thing. Family is one of the most important point in a Ukrainian female’s life, and she will certainly do whatever possible to make her home loving and satisfied. Ukrainian sweethearts are likewise understood for being terrific other halves and mothers. Be yourself: Be on your own while you are dating a solitary Ukrainian woman. Unfortunately, there have been records of Ukrainian women using dating websites and apps as a method to target innocent targets for financial gain. However, there are a few key differences that you need to be mindful of.

Now you know numerous realities regarding local dating culture, so when you make a decision to fulfill Ukraine woman, utilize the suggestions we have actually supplied, and you are ensured success. Beautiful females from Ukraine will be able to hold smart discussions on numerous topics, which is something that numerous guys discover extremely eye-catching. Women from Ukraine can hold smart discussions on numerous subjects, which is something that several men locate very attractive. Dating in Ukraine is similar to most Western countries. Read on these location-specific Ukraine dating tips for your simple guide. Create an attractive account: You require to produce an account that looks fascinating and excellent enough to bring in the interest of females from Ukraine. Keep all sensitive conversations private until you charmdate review feel safe and secure adequate moving on with a person passionately and see to it no one else has accessibility to those chats either. Generally, possible Ukrainian new brides candidates should beware when selecting a company and ask those delicate difficult concerns prior to getting on an aircraft or handing over a great deal of cash for that ‘special girl’. Be a gentleman: Be a gent while dating a Ukrainian lady. If you reveal on your own as a positive gent experienced in dating Ukrainian ladies, you can win a nice bride-to-be from Ukraine.

If you take place to be in New York City, Internations will set a schedule to satisfy fellow Ukrainian nationals in the city. They do their best to set one of the most fine-looking photo to their account to make you, man, interested. Ukrainian women desire to make an excellent impression and show you their finest side. Ukrainian women are stunning and draw in guys from around the world which is not a new fact for them. Thus, there are a great deal of intriguing realities about them that you might not understand about. Most solitary Ukraine ladies are currently there on this website. Upload your recent photograph on the account, as women from Ukraine favor to day open-minded males. Female empowerment has been on the increase in Ukraine, with more and even more campaigns being released to assist close the gender gap in education and job opportunity for ladies. They are a lot more likely to intend to have kids and be stay-at-home mothers. They are much more womanly and mild and deal with their appearance greater than Western women. They deal with their appearance and constantly look their best. Complimenting a female on how she deals with herself or what an amazing person she is will win you brownie factors with her.

This article will certainly give you some tips to help you make your dream come real if you are dreaming of getting a Ukrainian woman for dating. Therefore, if your partnership with a Ukrainian lady is necessary to you, consider prioritizing it. However, if you live away from Ukraine, you may be questioning: how to fulfill Ukrainian woman as a foreign person? While online dating is a wonderful means to attach with Ukrainian women, it’s vital to plan to fulfill in individual eventually. Before you sign up with any kind of website for dating Ukrainian females, obtain acquainted with the services and features it offers. Teamo uses a twist to typical swiping apps like Tinder by supplying a “Maybe” option. You have to find a genuine and trustworthy web site that supplies Ukrainian females on the internet dating. Sexist statements. The truth that you’re a handsome international guy doesn’t mean that a Ukrainian female will certainly agree that she should sit in your home, chef borscht 24/7, and increase kids. They will be able to hold intelligent discussions on various topics.

You’re actually a just right webmaster. The website loading velocity is amazing.

It kind of feels that you are doing any unique trick.

Furthermore, the contents are masterwork.

you’ve done a fantastic activity in this matter! Similar here:

tani sklep and also here: Najtańszy sklep

What is a Serious Relationship? But, with time solely the relationship is left behind, with little or no happiness. One technique to befriend such a person is to take the time to listen to them. Another key profit to relationship administration is the way in which it might scale back risks. That is where a Customer Relationship Management (CRM) system comes into play, serving to you streamline your interactions with prospects and revolutionize your small enterprise. Automated procedures within a CRM module embrace sending sales team marketing materials based mostly on a customer’s selection of a services or products. Ultimately, CRM serves to enhance the shopper’s overall expertise. CRM purposes additionally allow corporations to supply timely, correct processing of buyer orders and requests and the continuing management of customer accounts. Customer relationship administration consists of the ideas, practices, and guidelines a company follows when interacting with its clients. International Journal of information Management. Joking Relationships” Can End Serious Conflicts, DePauw Political Science Professor to inform International Political Science Colloquium in France”. Or, if the related relationships have already been defined on all of the fashions concerned in the relationship, you might fluently outline a “has-one-by means of” relationship by invoking the by way of methodology and supplying the names of these relationships.

When you wish to customize the keys of the relationship, you might cross them because the third and fourth arguments to the hasManyThrough method. Next, on the Tag model, it is best to define a method for every of its attainable mum or dad models. The nub of the “family†amendment is to extend the constitutional that means of household to what are termed “other durable relationshipsâ€. If relationships between unmarried people are to be the constitutional basis of families in future, we should ask whether they embrace what are actually termed “single-father or mother familiesâ€. The so-referred to as “care†amendment would additionally delete provisions of the Constitution which have prior to now been relied on by the Supreme Court to invalidate revenue tax laws that had been discriminatory towards married people and in holding that husbands with enough means couldn’t demand that mothers be obliged to work outdoors the home the place it was their selection to look after their youngsters.

With extra reliable data, their demand for self-service from companies will decrease. Jokes apart, there are some reputable (and more legitimate) purple flags that actually should not be ignored. 57. “There isn’t any problem strong sufficient to destroy your marriage so long as you are each keen to stop preventing in opposition to one another, and begin combating for one another. That order can’t be made unless the court docket considers that correct provision has been made for the spouses and youngsters of that marriage. While that might sound uncontroversial, what happens if a single lady and her little one constitute a family – and an [url=https://asiamescam.wordpress.com/]asiame.com scam[/url] unmarried man joins the family and they’ve two further kids? Moreover, society can easily distinguish between the family rights of people who are social gathering to relationships by reference to their marital status. Check in with people when you might want to. You want to recollect, that you just enter right into a relationship to be completely satisfied, and also you should be! Remember, belief takes time to construct, but it is crucial for the survival and success of any relationship, especially a protracted-distance one.

The difference between a military LDR and an everyday LDR is that, while the common LDR there is extra communication the military LDR communication is unexpected and managed by navy regulations or there is just not much time to speak. These tiffs might give rise to common conflicts which shouldn’t be allowed to continue. It takes time to present and get time, so be affected person. You’re disrupting the cycle of negativity and refusing to provide it any gas to proceed. It takes a number of spokes to hold the wheel together and the wheel is what helps move the initiative along. You may hold onto some of it, however most might be spilled. This typically entails a person feeling as though they’ve a close, intimate reference to somebody whom they have never met as a consequence of closely following that particular person (or character) in media, similar to Tv shows, videos, podcasts, and so on. For instance, a baby could really feel as though they are buddies with a fictional character on account of steadily watching the character on a show, or a fan may feel as though they have a relationship with a pop star because of their emotional investment in the star’s career and life.